Discover more from Unhedged Updates

Unhedged: FX HedgePool & Re-Visit Prime Broker Concerns

I've now seen a few articles this summer about FX HedgePool's product, which is quite interesting given our past discussions about the CFTC's critical view of prime broker models (https://www.fxhedgepool.com/)

“I don’t do links. Explain FX HedgePool, with gifs.”

FX HedgePool focuses on the buyside and providing a “peer-to-peer order matching” service, which is intended to limit price movement caused by a new order made with a dealer. Instead, the idea is, if you cut out the dealer and just connected the buyside with the other buyside (Speculator? Trader?), you remove the spread and execute at the prevailing market rate, (rather than a market rate impacted by (a) your order and information leakage, and (b) also incurring a spread).

However, here's the twist: while FX HedgePool aims to facilitate peer-to-peer trading, it still involves a dealer in the middle to service as a credit intermediator.

Reminder: Where is the CFTC with Prime Brokers?

If you remember CFTC Advisory Letter No. 21-19 and CFTC Letter 23-06, then just keep on your merry way to the next section. If you are new to these emails or want that refresher, go to the heading below “Refresh: Prime Brokers vs CFTC” at the bottom of this email, which is copied from a June 2023 email. As an update, no letter mentioned in 2023 has been updated…not even the two from 2013. Shocking, I know.

FX HedgePool & Credit Intermediation

While the peer-to-peer idea has some obvious benefit, one major issue: No buyside desk trying to hedge FX risk for their huge company wants to explain why they were doing millions in hedging with “Ummm, some other rando I met on ISDA-Tinder, convinced to join FX HedgePool and promised me they had the goodest credit.”

They want to name a bank/dealer, and have that likely be the bank or dealer with whom their company conducts most of its financial transactions. They need to trade not only with a recognizable name that gives the trader credibility and air coverage, but the buyside also needs to trade within the company's policies or restrictions, which may only permit FX hedges with certain entities.

That list of certain entities, is unlikely to include the other “P” in “P2P”.

This is where we can appreciate the magic of FX HedgePool: They have banks on this P2P platform that offer credit intermediation between P and P, and also provide booking and settlement services (and I would expect trade reporting and basically all the other items non-bank/dealers want with a bank/dealer counterparty).

Also, if you were FX HedgePool and trying to get new users: This set-up means FX HedgePool gets to leverage existing ISDA and FX Master Agreements that a bank/dealer may already have, rather that requires fees and expenses of re-papering existing+working trading relationships.

Now, FX HedgePool’s “customers” are all customers of its bank/dealer’s providing credit intermediation. Work smarter, not harder.

Why would a Bank/Dealer help FX HedgePool?

Good question. For one, they do get paid what we’ll call the Credit Intermediation Fee. The second reason, maybe the thinking of: If I am not the first to offer this to Counterparty-X, someone else will, and I could lose business, even though the products available on FX HedgePool are currently limited.

Credit Intermediation Fee

Nothing I found goes into specifics beyond noting that the credit-intermediary bank/dealer is paid a fee. Maybe that set-up is not too far different than generic prime broker arrangements.

If You Ain’t First, You’re Last

One reason you don't see the entire buyside business moving to FX HedgePool is that, based on various articles about the product, the ideal customer for this service is (1) a specific type of client—namely, those with a very predictable FX order flow—and (2) a client who can only execute a limited range of FX products (FX Forwards (?), FX Swaps and FX Spot).

If that is the case, perhaps bank/dealers see a benefit in engaging with counterparties who have significant flow business, suggesting, "Hey, we have an idea that can save you money on your execution costs for this flow work," with the expectation that such a tailored service positions the bank/dealer favorably for more profitable one-off or bespoke transactions with that client. Additionally, this could lock in the bank/dealer for 100% of the order flow, whereas previously, they had to compete and execute less than 100%. In this scenario, the Credit Intermediation Fee might be greater than the income from competitive business, or the certainty of “we will get 100% of this flow work” (and the associated predictability of counterparty interaction with the market desk) might be expected to yield a higher ROI that the current status quo.

Note re Pre-Hedging

Proponents of FX HedgePool (and any P2P model) would also point out that buyside firms with predictable flows are prone to "pre-hedging," which can negatively impact their pricing. There's some truth to this, but positions taken in anticipation of an order can also result in better pricing through a tighter spread, as dealers are more confident in their pricing ability versus slippage.

However, if that buyside counterparty frequently contacts multiple firms for indicative pricing (or if multiple firms anticipate this call based on historical patterns), the broader market might try to win the business by taking positions in anticipation of the order. This could negatively impact the buyside's pricing. But, in my opinion, this is somewhat the buyside's fault/responsibility, unless explicit instructions are given to the banks/dealers to refrain from any pre-hedging.

FX HedgePool: Limited Products Types (Regulatory Reasons)

Anyway, it's not like FX HedgePool is targeting the entire FX business. It serves a limited type of client and offers a limited range of products. Initially, the products were focused on FX swaps (though I couldn't determine if this term was used generically to describe any non-spot deliverable FX product, such as FX Forwards or FX Swaps). Recently, and this is how it came to my attention, FX HedgePool expanded to include FX spot trading with its new service, X•Bridge.

Here is why much of the issues/discussions associated with “Prime Brokers vs CFTC” does not apply to FX HedgePool: They are not facilitating the execution and credit intermediation of swaps.

Yeah, they are not “swaps” for CFTC purposes (thank you 2012 Dept of Treasury). For the business/traders wondering how this nuance plays out in other areas: This is why never worry about CFTC/PR margin rules for clients only doing FX forwards, FX swaps and FX spot trades. The CFTC has even stated HERE that a platform/system which only provided for the execution of FX forwards and FX swaps, then SEF registration would not be required.

FX HedgePool Will Not Takeaway Other Swaps Business (Today)

The regulatory constraints bring us to this point: FX HedgePool, under current regulations, has limitations on what it can offer. I doubt they are considering expanding their product line to include NDFs, FX Options, or other swaps. While they might be interested in doing so, they have to consider questions like, "Do we need to register as a SEF? And regarding the credit intermediation component, how do we justify that this shouldn't trigger DCO registration requirements for any of our credit intermediaries?"

Answering these questions and structuring a product to avoid registration is possible, but it requires careful drafting and structuring.

Commodity Swaps: Credit Intermediaries

I'd like to note that there is an asset class where (1) some form of "P2P" does seem to exist, (2) it's not uncommon, and (3) it deals with swaps: the commodities space, specifically in power. Here, a power generator (often the borrower in a project finance deal) may find another power company that can offer great pricing on a power hedge.

The issue: The Loan Agreement will limit the "Permitted Commodity Hedge Providers," and these are likely restricted to Lenders and their Affiliates or other highly rated financial institutions.

The solution: "Sleeves"

At least that is the term I hear used when this structure is described and executed. A Permitted Commodity Hedge Provider agrees to "sleeve" the transaction, which involves minimal work on their part, as they simply take both sides of the trade.

For various reasons, when I've encountered these in practice, I don't think they raise regulatory issues. No Permitted Commodity Hedge Provider is actively soliciting this structure. Instead, it usually occurs because the Borrower-Power Generator has sophisticated advisors who can lead the process of finding the power company and presenting the structure to the Permitted Commodity Hedge Provider. There are other considerations, of course, but since no one is actively marketing this structure, I don't think there are DCO registration concerns. However, that's just my opinion (and not legal advice, as a full analysis would need to consider all facts and circumstances).

Refresh: Prime Brokers vs CFTC

Now, a new topic but still in the FX markets: The below, this is about how the CFTC is chipping away at what is commonly referred to as European FX Intermediated Prime Brokerage Arrangements. This may present an opportunity for US liquidity providers because the US buyside may find there are fewer European liquidity providers it can access for FX transactions through the European prime broker arrangements (e.g., Options and NDFs, or any other FX trade that is a “swap” for CFTC purposes). The short summary of where we are and how we got here is below, but this email is probably more helpful as a “save for later reference” email, if this topic arises.

Condensed Version & Purpose of this Email:

Business Readers: Probably going to be harder for US persons to engage with European liquidity providers for FX Options and NDFs if those liquidity providers are not CFTC-registered Swap Dealers. I say this, in part, because it’s not uncommon for a non-US swap party to have a policy of “No US Persons”, simply because that does make life easier for them and keeps their legal fees much much lower from engaging with US counsel. I am not sure what impact there would be on deliverable FX Forwards and FX swaps, since a non-US liquidity provider can execute those all day everyday with US persons and never register with the CFTC as a Swap Dealer…but if the policy is “No US Persons”, maybe that distinction is not made. I’ll leave that to our European readers. Big picture: The European FX prime-broker arrangements helped the non-US entities engage with US persons, but in a way that kept them from worrying too much about CFTC registration issues (because the non-US entities never have a swap with a US person). Now, however, we are not sure how that model will hold up. The current CFTC staff does not like the model, even though the CFTC staff seemingly blessed it in 2013.

Legal Readers: If you’re familiar with the European FX prime-broker arrangements, and you are the prime broker, probably worthwhile to kick the tires. You do not want the CFTC to kick the tires for you. If you are not the prime broker, but sure do enjoy using that set-up….it will be interesting to see how much longer it lasts or how it evolves. It’s hard for this model to exist, include Options and NDFs, and the Prime Broker then not also be a CFTC registered Swap Dealer. Also, the below summary is more for you.

Background: 2013 CFTC says “We will deal with you later.”

In 2013, the Gensler-led CFTC took the approach of “Let’s make rules, see what breaks and fix it by issuing no-action letters and promising a future rulemaking to address whatever new issues come up.” I am still waiting on the rulemaking for Guarantees of Swaps. Anyway, one example is related to the European FX prime-broker market. Here, a US person could access liquidity providers in Europe via a prime broker. This presented a number of regulatory issues, so the CFTC issued No-Action Letters 13-11 and 13-39, which effectively bless the European prime-broker model subject to the conditions provided therein as “If you operate within these parameters…all is good.” These are also great examples of “Regulating through the Back Door” – i.e., when we effectively get “law” but it is not from the process of a rule proposal, comment and final Commission vote. No matter how you cut it, the negative is that the period of public comment does/should help craft law that adds value to the market and creates transparency (yes, there are costs, but ideally the law passes because overall value add exceeds those costs).

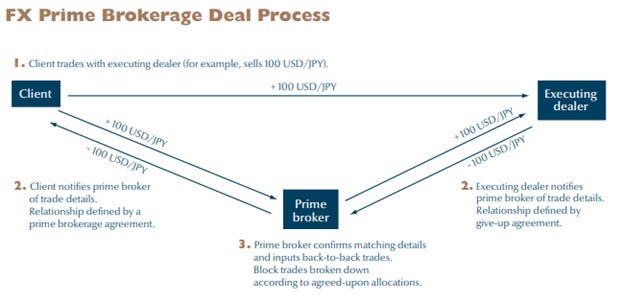

Anyway, No-Action Letters 13-11 and 13-39 were to remain in-place until a final rulemaking. Spoiler: Ten years later, no rulemaking has happened. Letter 13-39 describes the model under “Description of FX Intermediated Prime Brokerage Arrangements”, and even the Fed’s FX Committee gives us nice pictures HERE (but no gifs). But to simplify it, if you think of a cleared swap between two clearing members (so no customers), you get the basic triangle picture below, where a Prime Broker intermediates the trade. However, there is never a swap/FX trade between the “Client” and the “Executing Dealer”…instead, there is a process/understanding that the offsetting trades can be executed at and by the Prime Broker. Also, the Executing Dealer is often able to market/solicit the Client directly (or through an intermediary+agent of the Client, such as a broker). This was also known and ok with the CFTC, so it appears, from the 2013 letters.

Still Bored: Why Care?

Listen, this summary isn’t getting much more exciting. I’ve mentioned two No-Action Letters, hyperlinked to a Harvard article and am about to talk about SEFs and DCOs. Go get a coffee, or read this when you have 5 minutes to learn about this subject just enough to be able to confidently say "Good question, the prime broker and CFTC issues are complex. Let me circle back.”

Prime-Broker, Bad. SEF/DCO, Good.

Now, to be fair, in this model it’s not unfair to say that the Prime Broker might as well be a SEF, DCO or both. It is facilitating transactions which originate from discussions between two other parties, and those discussions then result in two offsetting swaps, to which the Prime Broker provides credit intermediation. So the CFTC’s view today (discussed below) is not completely out of left field. However, if you said the Prime Broker was a SEF, I would also point out that the prime broker is the only counterparty…so they operate a “one to many” platform. It’s pretty clear from the CFTC’s rules (as opposed to staff guidance) that this is not a SEF. As for a DCO…this is Europe. They have a completely different clearing model (Principal to Principal) versus the US model (Agency-model, though the S&C opinion challenges this). I could appreciate lawyers familiar with the European model not immediately seeing a clearinghouse unless you really just say all customers are clearing members. However, even if you concede that point, there is never a swap being novated/transferred to the Prime Broker aka clearinghouse, which seems to be a critical part to any clearinghouse (though I guess the CFTC would place little distinction between (A) a swap being novated/transferred versus (B) a non-legally binding mutual understanding that two parties will enter into two offsetting trades with a prime broker, particularly gives the CFTC’s broad powers regarding evasion).

Today: Today’s CFTC disagrees with the 2013 CFTC?

Yep. First, there was CFTC Advisory Letter No. 21-19. Now, if Person A is helping facilitate a swap between Person Z and Person Y, Person A will need to consider SEF registration. Shot #1 at the Prime Broker (and, to be honest, probably leaving CTAs like Chatham, Kensington, Riverside, Bascom Advisors and others very confused given what happened HERE).

Pause here to remember: Yes, these advisory letters should not serve as the basis for enforcement actions (again, see “Regulating through the Back Door”)…but they do.

Just last month, we got CFTC Letter 23-06. It is essentially saying that many (all?) Prime Brokers operating under the 2013 business model are DCOs. The letter noted that the CFTC’s Division of Clear and Risk (“DCR”) is “focused” on the first part of the three-part analysis for determining whether a particular entity is a DCO. Sure sure, they also say this: “While DCR staff does not believe that all prime brokerage arrangements will meet the definition of a DCO, DCR has recently informed several SEFs and SEF applicants that proposed market structures requiring use of a single prime broker that is a centralized credit intermediary would be required to register as a DCO…” DCR is just focused on arguably the broadest prong of the analysis…so when I read “does not believe that all”, I also think:

Anyway. What was ok in 2013 is likely not ok today, and not because of any rulemaking coming to fruition, but because different people are in charge. It is unfortunate that we get here without a formal rulemaking procedure and that the more recent letters give no indication of what (if anything) changed since 2013. Honestly, even the CFTC saying that certain facts were not presented in 2013, which the CFTC believes would have been material, would have at least reiterated the importance of stating all material facts when asking for guidance/relief. However, even if that is the case…the “bad facts” are alluded to in Letter 13-39 when it describes “the most basic form of prime brokerage prevalent in the market”. So, really, it seems what was ok for CFTC staff in 2013 is not ok for CFTC staff today.

Moving forward, the last two CFTC letters will probably rule the day for the next 10 years or more.

Subscribe to Unhedged Updates

Updates regarding swaps, derivatives and the financial market more broadly...but with gifs.