BSBY/AMERIBOR - Not a Great July 4th

BSBY/AMERIBOR - Not a Great July 4th

We’ve discussed a few times here the various “credit sensitive rates” which were new reference rates that tended to more closely align with LIBOR. The most common seemed to be BSBY and the best named was AMERIBOR, a rate that I always associated with:

Well, IOSCO was definitely not enjoying Myrtle Beach and the tastes of freedom last week, but instead was issuing press releases HERE that based on their review of the credit sensitive rates (e.g., BSBY and AMERIBOR), “Administrators, as well as their auditors and independent consultants, should refrain from any representation that the CSRs reviewed are ‘IOSCO-compliant’”. (emphasis added) From various other sources, while the release does not expressly mention BSBY or AMERIBOR, these were the two credit sensitive rates receiving the heat from IOSCO.

What is weird here: IOSCO doesn’t have any actual legal authority. No one is going to jail for using BSBY or AMERIBOR – i.e., they cannot deem a rate “not IOSCO compliant” thereby outlawing its use. IOSCO sets principles, then someone like Bloomberg hires an auditor to review their rates and determine whether, in the opinion of the auditor, BSBY satisfies IOSCO’s principles. In fact, that is exactly what BSBY did do. So now we are in this weird space.

Why does this matter?

Early in the LIBOR Transition, common fallback language (including in Term SOFR documents) included fallback triggers based on IOSCO compliance. Eventually this was removed from the LSTA published document for Term SOFR (which makes sense, because, as noted….IOSCO compliance is more akin to an opinion that people can disagree about, and not a formal legal determination IOSCO makes). A lot of BSBY-Fallback Language from an EDGAR search appears to be triggered based on “Bloomberg or any successor administrator of the BSBY Screen Rate or a Governmental Authority having jurisdiction over the Administrative Agent or Bloomberg or such administrator has made a public statement…that BSBY or the BSBY Screen Rate has failed to comply with the International Organization of Securities Commissions (IOSCO) Principles for Financial Benchmarks”.

Given the lack of AMERIBOR’s use in publicly syndicated deals, we can’t really provide a good sample set here, but I would anticipate something similar there, so we will assume that is the case for our purposes (but people will always need to read the contract, regardless of the reference rate).

Per BSBYWatch, there are 175 syndicated loans out there tied to BSBY. Also, BSBYWatch is something we have referenced here before as a site with statement to take with a grain of salt because they will support BSBY, but right now it can also serve as a place to stay abreast of (i) possible responses to an examiner to support the continued use of BSBY and (ii) how Bloomberg responds to IOSCO (if at all).

Does this trigger Fallback Provision in BSBY/AMERIBOR Loan Documents?

Seems to be a good argument that IOSCO’s press release does not trigger fallback language, since IOSCO is not a “Governmental Authority” (though always check your loan documents) . It would require a little more…it requires the Administrator for the rate (Bloomberg or AFX) or regulator (e.g., a bank regulator) to come over top.

Regarding a possible statement by the Administrators…it will be interesting to see how this one plays out.

IOSCO, because it is not a governing body with power of law/enforcement, can state that people “should” refrain from certain representations, but reasonable minds can disagree such that Bloomberg (I expect) could just as easily say “Thanks IOSCO, we hear you but based on our data and your principles, we do believe BSBY is compliant with IOSCO’s principles and will leave it to our users to come to their conclusions about whether to use this rate and it’s IOSCO compliance.” I just wonder if they will be able to find an auditor to re-affirm a statement regarding IOSCO compliance.

Which brings up another interesting point: Bloomberg’s webpage and PDF which represented IOSCO compliance is no longer available (HERE or HERE). You can use the Wayback Machine to see what it used to say, but that is of little help here. So for the here and now…we do not really have anything from Bloomberg (based on our search). AMERIBOR’s statement regarding IOSCO compliance appears to still be available HERE.

In BSBY’s defense, IOSCO issued this statement but issued no detailed support for their conclusions. It is actually pretty unusual here because the statement by IOSCO references a “Review” that supports their conclusion, but we cannot find it anywhere. Also, we would be curious to know how something like BSBY, which is based on the commercial paper market, has too few transactions…but Term SOFR, which is based on transactions in SOFR futures contracts and overnight swaps, underpins what seems like the majority of business loans (and related swaps), but is IOSCO compliant? I’d just like to see how they threaded that needle.

What about BSBY/AMERIBOR Swaps?

Do people do these? Joking, but not joking, because if I am a borrower doing a loan, that I want to hedge, the lower Fixed Rate will be on a SOFR-based swap. With that said, the IOSCO statement is not triggering ISDA’s fallback language. That generally requires a statement from the Administrator or a regulator stating that the Administrator has ceased or will cease to provide the Credit Sensitive Rate permanently or indefinitely.

Continued use of BSBY/AMERIBOR?

In short, I don’t think IOSCO’s statement means “BSBY and AMERIBOR are not IOSCO compliant”…it just means that IOSCO disagrees with those who think it is compliant (admittedly, this is from a strong source to make that determination). For Lenders, the question now is whether that means anything for fallback provisions. It also increases the heat on their continued use. I still think a bank’s balance sheet is well served by having some exposure to credit sensitive rates to mitigate the risk that the Fed steps in to lower SOFR below the cost of funds (like we saw at the start of COVID), but banks will also need to think about how to respond to examiner’s question of “Why are you using this rate that IOSCO said was not compliant?”

Today, part of the response may be something akin to “Correct, IOSCO made that conclusion, but did so without giving any detailed support. However, the Administrator for the rate has provided us a detailed support for its conclusion regarding IOSCO compliance which does appear convincing.”

The Bank Policy Institution Predicted this Risk and Did Not Like this Press Release Process

BPI did allude to this risk of IOSCO non-compliance but also picked-up on the nuance that this is not some determination made by IOSCO or public press releases by Gary Gensler, where BPI concluded HERE “From the foregoing analysis, BSBY does not appear to be subject to manipulation or present a financial stability risk, but if government agencies believe that it or some other reference rate is fatally flawed, then the appropriate process for taking such action is a regulatory one, with prior notice and public comment by the affected parties (presumably including the people in the business of publishing the benchmark, as well as borrowers and lenders) — not a non-public process using examiners to direct individual firms to avoid that benchmark.”

Other Credit Sensitive Rates – e.g., AXI

The rates reviewed by IOSCO were CME and ICE’s Term SOFR Rates, BSBY and Ameribor. It does not include AXI, which is a credit spread add-on to SOFR which has the impact of causing a SOFR-based rate to now include a spread adjustment that effectively gets SOFR to a place where it acts more like LIBOR.

UPDATE (2:12pm July 11, 2023)

Quick update from BSBY and AMERIBOR.

HERE from Bloomberg. HERE from AFX. AFX is taking IOSCO head-on, essentially noting that their principles are “open to interpretation”, IOSCO is “not a regulatory body” and even noting that despite IOSCO statement’s that “IOSCO had not conducted any annual reviews of CSRs, leaving it to the individual firms to complete self–assessments.” AFX notes it will “sufficiently address” IOSCO’s concerns.

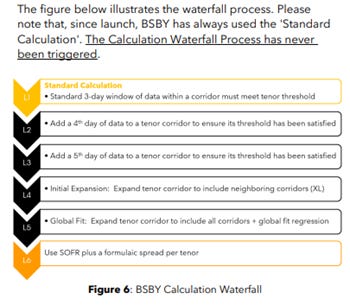

Bloomberg does not expressly address IOSCO, but re-iterates the rate’s resilience, including how it performed through the March 2023 financial stress on regional banks and re-iterates the waterfall process during low transaction volume (essentially, BSBY becomes a rate that is based on SOFR plus the historic spread between BSBY and SOFR):

Anyone looking to have information on-hand to explain why IOSCO’s press release is not a Level 5 alarm, these should help!